Favcy Review: June 19th, 2021

.png)

Between a Venture Builder, a VC and the Private Equity guy — who is the coolest?

You can stop here. None. A Founder of a Startup is the coolest.

But if you still insist, do not like click baits, are ready for some exhaustive reading that separates the chaff from the grains and want to understand the nuances that differentiate the three — please go ahead.

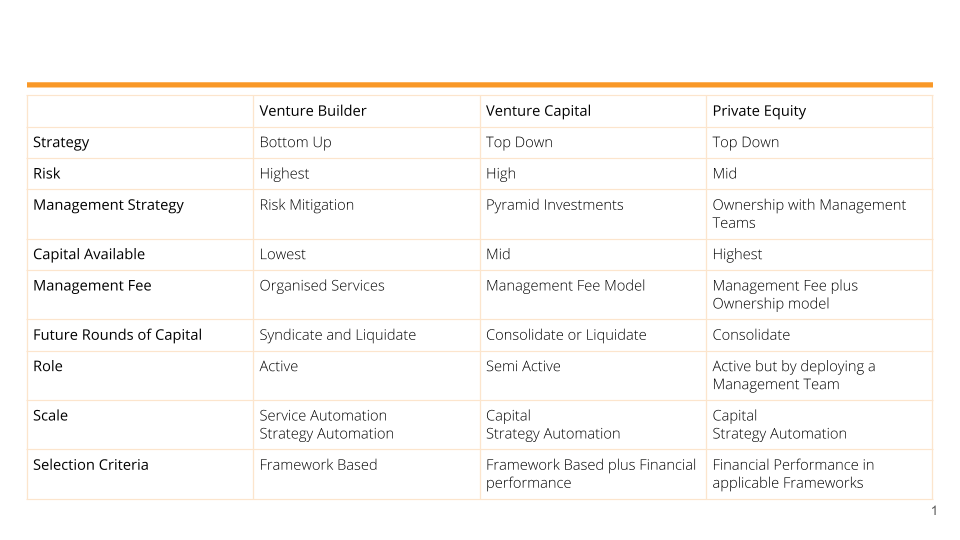

- Let’s start with Strategy

For a venture builder (VB) the strategy is going to be bottom up. What I really mean is that the venture builder would be working very closely with the founders and would be creating value with the founders by almost being a co-founder with them. Because VBs do not operate on hefty management fees, they have to generate value for themselves and for their portfolios in which they have taken positions. More often than not, you will find VBs taking equity from the founders and then getting parts of the acquired equity underwritten by their own partners or a group of Angels. So now you know how VBs survive. In my opinion, the coolness quotient is going to be very low here. If you are planning to be an analyst at a VB firm, roll up your sleeves. It’s bloody hard work.

Venture Capitalists or in short VCs will be having a top down strategy. They will be raising a fund from Limited Partners and will be deploying in assets which they believe will become, (you guessed the word) Unicorns. That’s a bit exaggerated, but yes, they need companies that are space missiles and where their capital not only counts but also creates a moat. Pretty cool right!

Private Equity folks also have a top down strategy but they deal with larger companies because they invest large sums and they invest large sums because.. That’s correct; they invest large because, they raise large sums from Institutional investors. And these guys come a little later in the journey to consolidate, create operational efficiencies and yada yada. A little less cooler than a VC but similar in coolness to a VB.

Coolness Quotient (CQ for strategy)— |VC 3, PE and VB 1 each

2. How about analysing the Risk levels for all three ?

VBs operate in the maximum risk zone. So a few claps for them. They operate with idea stage founders and there is a report by UNDP, which says that the risk with idea stage founders is so hight that private players do not like to operate in this zone. Therefore the onus is on the Government to actually provides grants through incubators. Do not squirm on the word grants. There is a thought behind that too. Governments give grants to Incubators, in hope that few of them will become bigger and will be in a position to become legitimate tax payers. Unfortunately, building a startup requires more than just free money. We all know where the grants and the incubation model has gone, so VBs do a cool job here. Majority of evergreen funds or impact funds are looking to operate in the VB space or with VBs and the reason is clearly because of the impact that the VBs are having in the space of early idea stage ventures. Ting, that’s just a small noise for coolness points going up for the VB folks.

Does that mean, VCs and PEs aren’t taking risk? Absolutely not. But risk is very relative. IMHO, VCs take risk more than that taken by PEs but lesser than that taken by VBs. And it’s purely a matter of their business models. VCs will like a company in a space that they believe is virgin and will back founders post they have achieved traction. PEs like to come in with large dollars and help in organising the space through large capital deployment and by even introducing their own management teams.

Coolness Quotient (CQ for Risk) — |VB 3, VC 2, PE 1

3. Moving on to Investment Styles.

Venture Builders, co-build with some great founders, operate in a very high risk zone and have the moral responsibility towards the Angels that are underwriting parts of their risk. Their style, therefore is like an elder brother, sister — protective and that of a risk mitigator. You can smell a good Venture Builder from a distance. They will have frameworks and models that work for them and for their portfolios. And they will continuously try to mitigate risk to make sure that the portfolios can survive the proverbial valley of death.

VCs on the other hand are about raising capital, deploying, exits and therefore invest and think differently. Some of the smartest VCs that I have met or work with have a very clear understanding of the investment strategy that they follow. It’s sort of like a pyramid. Assuming you have raised x. Invest x/x in 10 ventures. Double down on three of those with X/7 and then go big on one or two of their winning horses by deploying the remaining capital. So if you are a founder, who is approaching VC for their fund and have read it in blogs, papers that it’s a 50Mn fund, remember you are vying only for the first 10 mn. It is bloody hard work to get the first cheque from VCs because post that, if you are performing well, they will double down on you. So life becomes a lot simpler.

Private Equity players also will have different styles but a prevalent style is that they come in with capital and they also bring in some management teams to help the company grow and consolidate. At the level of PE, it is not so much about the Founders but about the Brand and company and the market that they are looking to capture. It’s about building a large company that can be IPOed.

Coolness Quotient (CQ for Management Style) — Am a bit torn here. But let’s see |PE 3, VB 2 and VC 1

4. Capital Availability

Lots of laughter- Of course there is no capital to play around, if you are a VB. Every single move that VB advises has to be well thought out, structured, researched, tried and tested. VBs work most frugally. They have to. So no corner office or Business Class happening here. VBs provide organised services, take equity and they also operate in the highest risk zone, so how do these blokes literally survive? They survive and thrive (fortunately in case of Favcy, the VB that I represent) through providing immense value in the highest risk market. The value they provide is not only to the Founders but also to the Angels.

Angels are a crazy bunch themselves without whom, this ecosystem would not have moved an inch. So some polite applause for all the angels out there. Angels have capital to invest but that is limited in quantum. So they cannot follow the VC route of pyramid investing and therefore literally spray and pray (well most of them). Now VBs are a perfect playground for Angels to actively scout great deals. Because VB gets the best deal on a portfolio, Angels typically can create a pyramid structure of investment with the VB itself.

How does this work? Simple, If an Angel has y capital. Divide y/y and buy equity of say 10 startup portfolios that you like from a Venture Builder (it is called underwriting part risk) and then go y/6 directly in one or two preferred startups of your choice and then remaining deploy in the one that you believe is doing the most traction. Good VBs will have an Angel Network going with them. As an angel, you could reach out to them, they will not only provide you will deals, but also will offer you partner insights, monthly updates and will help in mitigating risk. They work on a symbiotic relationship and it works!

VC’s obviously have higher capital to play with than VBs but lower capital than that of PEs.

Friendly advice to some Founders. VCs unfortunately, cannot have place for emotions because of their deployment models and even though they may have capital reserves, they can only deploy with their best performing assets. So if you have a VC on board and you are not being able to convince them to help you with the next round, look closely at your business — Unit economics, positioning, market size, operational efficiencies. Maybe the problem is hidden there and not with the VC who is on your board.

As you progress in this blog, you will appreciate that the space that PE operates from is very different. It’s literally not investing in a startup (in true sense) but in a company that has shown great track record and has the potential to own a complete market. They come typically pre-IPO and have the strength and wherewithal to extract profit from such companies through their playbooks and their management teams.

Coolness Quotient (CQ for Capital) — Rating purely on the single point of ‘access to capital’ | PE 3, VC 2, VB 1

5. Revenues and Cash Inflows for the VB, VCs and the PE folks?

Full marks to VB for innovating and bringing a new model to the capital industry. So here is the inside scoop. VB unlike VC and PE does not survive on Management fees from the funds that they raise. In fact, they are in the pure business of buying and selling equity. What is interesting to note is that as VBs work with the riskiest ventures, which are at an idea stage, they are able to buy equity against the organised services that they provide. And they are then able to sync up with Angels, who buy a small percentage of the portfolio’s equity but through a VB. This buying of equity and then selling a small part of that equity is what keeps the revenues ticking for a Venture Builder. As you may have calculated, the upside for a VB is the portfolio’s future performance and how the equity across their portfolio performs.

Due to a steady revenue stream and a potential upside, you feel generally find VBs to be patient as they do not have the pressure of managing the life cycle of a fund.

VCs and PEs on the other hand work on Management fee basis. They create a pool of fund from LPs and then take a management fee plus take a carry over and above.

Management fee you would have understood. It’s a simple percentage of the fund size to pay for the management. But carry, in simple terms is a percentage of growth in capital. So in layman terms, when VCs/PE return the capital to their LPs or to their Institutional investors after selling their positions, then they can charge a certain amount of percentage over and above their committed return. That’s a carry. And you guessed it! That’s the only slight problem of the VC business. It’s a business of exits. Therefore do not expect VCs to be patient. They cannot be.

Coolness Quotient (CQ for Revenues and Cash Flows) — VBs win this hands down, because of their model, which is impactful and patient. | VB 3, PE 2, VC 1

6. Participation in future rounds of Fund Raise; Follow on strategy

A VC will invest in some good assets and then double down on the successful ones. Therefore for a VC, participation in future rounds of capital is an obvious corollary. But not all assets get second or third investments. The top ones will.

PE follows a different approach. At their level, they are quasi owners already and are like founders with deep pockets and a business that is working. So future rounds of capital, till an IPO is almost the most obvious conclusion.

VBs follow a different approach. Few of them like Rocket Internet are almost like PE folks, looking to venture build and therefore behave differently. But for the new age VBs, their DNA is very different and you will see them creating syndicates to lead in the portfolios that they would like to double down on. VBs creating a parallel VC fund is also an obvious growth trajectory.

Coolness Quotient (CQ for Participation in future rounds of Fund Raise)- PE wins this one | PE 3, VC 2, VB 1

7. Portfolio selection criteria and process

Let me start this section by asking a question. Which of the three would be handling the maximum load of inbounds? The obvious answer is the Venture Builder. The number of founders with an idea are disproportionately higher to the number of startups doing traction and more than disproportionately higher to the number of startups that now have a strong foundation and can reach out to a PE firm.

All three VB, VC and PE will have their own frameworks of selection. VC would like to scout for deals in the areas that excite them and then its about diligence. PE has a similar structure but because they are writing such big cheques, they can almost control the fate of a startup. VB on the other hand, will be working with a founder, in scouting an untaken positioning in a large market and unlike VC or PE, who do not have to make their systems of shortlist public, a VB worth its salt will keep the systems of selection public. The logic is simple, the more the founders use their systems to validate their ideas, the better founders a VB gets.

The net story is, all three will have elaborate systems of selection but not all will keep it in public domain or will articulate the reason of selection/rejection.

Coolness Quotient (CQ for Portfolio Selection )- VC handles great complexity with limited control. I’d give them the highest score on coolness here.| VC 3, VB 2, PE 1

8. Scale, Positioning and Defensibility

As we near the end of this gigantic and verbose writing piece, I’d like to congratulate you for your patience and would be glad to hear your views on the parallel startup side, that I have tried to simplify through this blog.

Scale and positioning are not only important for startups but are also important for a VB, a VC or a PE. They all are ultimately businesses that have to add value to stakeholders and then survive and eventually thrive.

I often cite this piece from ‘The Art of War’ by Sun Tzu.

_1.png)

You might want to re-read the piece. Its astonishing writing and literally talks of the two most important elements of a startup success. Positioning and Defensibility.

VBs, VCs or PE are no exception to the above rule. While they all find their positioning, through their brand promise and the values that they offer, they also continuously need to work on their brand and their promise to build defensibility and moat.

IMHO, a VB outscores both PE and VC on this. A VB literally is in the business of providing organised services for equity and then selling parts of it within its ecosystem and it can massively scale by automating the service line. That’s unfortunately not true in case of Capital. For both VC and PE, the brand that they build and the capital that they raise and keep raising lead to scale and defensibility.

Having said that, it’s no chid’s play to automate Venture Building assembly but if a VB is able to achieve that level of sophistication and automation, they have a definite edge on defensibility. In fact, visualise a world where startups can actually shoot their idea, find a positioning, get a digital product and get frameworks of traction all in one or two sittings. See, that’s automation of a Venture Building assembly line and the thought of it is orgasmic!

Coolness Quotient (CQ for Scale, Positioning and Defensibility)- VB — no questions asked| VB 3, VC 1, PE 1

Hope you enjoyed the piece. Let me know. And I am really not bothering to tally up the scores. You may, if you want. The intent was that I could simplify the capital ecosystem for you and help you in building a great company that you deserve to build.

Stay tuned to receive the latest industry trends, investor insights, our exclusive angel bytes, and much more!

A platform for first-time angel investors to learn the science of early-stage startup evaluation. Get exclusive access to pre-vetted deal flow and make your first investment.

Reach out to us: