Have you heard of zombie unicorns?

Dear Reader, do you like zombie-apocalypse movies? If you're familiar with the genre, you must be aware how zombies are portrayed to be half- dead, brain-less monstrosities that are only hungry for blood. A recent Reuters report claims that some unicorns in the Indian startup ecosystem might be turning zombie. It was a no-brainer (pun-intended) that we had to find out what zombie unicorns are. So we decided to get to the root of matter.

This week in Favcy Review, we are exploring this neo concept of "zombie unicorns" and investigating startups that can potentially turn zombie. Read on to find out!

In other news, in this week’s CurrentOpenDeals section we present to you *drumrolls* -CompassTot, an early childhood education platform that takes the guesswork out of raising a toddler. It enables parents to build a solid foundation for their 2-6 year old kids via fun, personalised activities in byte sized format.

The Future@Favcy section has open positions here at Favcy, in case you’re looking to join our boat!

Lastly, in Angel Bytes we’re explaining different kinds of investment instruments for angel investors.

Do share your feedback on this effort. You can mail us at insider@1stcheque.com

Cheers 🍻

Ninie

Come join our table!

The Favcy Family is growing faster than ever. With new investors joining us each day, the Opening Day allocations have started filling up faster. We have been swarmed with requests to increase the allocation pools across our portfolio startups. We hear you.

The 'Current Open Deals' section gives you access to deals that previously weren't available! From allocations in the latest deals to spots carved out just for you in growth-stage startups, all the information you need is here! An exciting investment journey lies ahead.

This week, we have CompassTot in the house!

CompassTot is a platform at the product stage which enables parents to build a solid foundation for their children aged 2-6 years through personalized fun activities in a byte-sized format. CompassTot offers a unique solution to millennial parents who face problems such as information overload and lack of time when it comes to figuring out the right things to do for their children.

We are delighted to inform that we bring this opportunity to you at its 2nd Cheque because the entire 1stCheque round got subscribed to before we even had the chance to organize an Opening Day with the Founder!

Here's what Ajay Dadheech, an investor in CompassTot, has to say about the stellar opportunity -

In 2022 the estimated size of the Early Child Care and Education market in India stands at US$ 80Bn. The sector accounted for spending of US$ 32Bn in 2015 and has since been growing at a steady pace of 25-30% year on year. An estimated 80% of the urban 2-6-year old education and care market is currently unpenetrated.

Check out CompassTot's investor dossier to find out the secret sauce that shall establish CompassTot as a market leader and create a ubiquitous platform connecting stakeholders in India’s Early Childhood Care and Education market.

Stage: Product Ready | 2nd Cheque

Industry: Early Childhood Care & Education

Access the Investor Dossier here

Access other Current Open Deals here

Looking to become a part of a work-culture that is inclusive, transparent, and experience the joy of working together to create something wonderful? We’re looking for people who are as excited as we are to help build our vision. Come join forces with us!

Currently, we have these openings:

1. Project Manager - Apply Here

2. Product Manager (1stCheque by Favcy) - Apply Here

3. Investor Relations Associate - Apply Here

4. Content Writer Intern (INBY) - Apply Here

Check out all the other openings here!

Dawn of the Zombie Unicorns?

By Ninie Verma, Content Associate, 1stCheque by Favcy

- India getting its first unicorn in 2011 to the country completing a century of startups valued at a billion-dollar or more in almost a decade is no mean feat.

- But what if we told you that a new wave of "zombie unicorns' might be around the corner?

- This week in Favcy Review we dive into the state of unicorns in India, the recent funding slowdown and the possible birth of zombie unicorns.

Read on!

The Index for Investment Instruments

By Ninie Verma, Content Associate, 1stCheque by Favcy

- There is a wide range of investment instruments that angel investors can utilize when investing in startups, but do you know about all of them?

-

From CCDs to CSOPs, this week in the Angel Bytes section we bring to you an index of investing instruments and explain each one!

Read away!

CSOP, CCD, CCPS - you must’ve definitely come across these terms and more. There is an abbreviation for everything in the innovative world of angel investing! Here is an index of investment instruments to help first-time angel investors understand each one better!

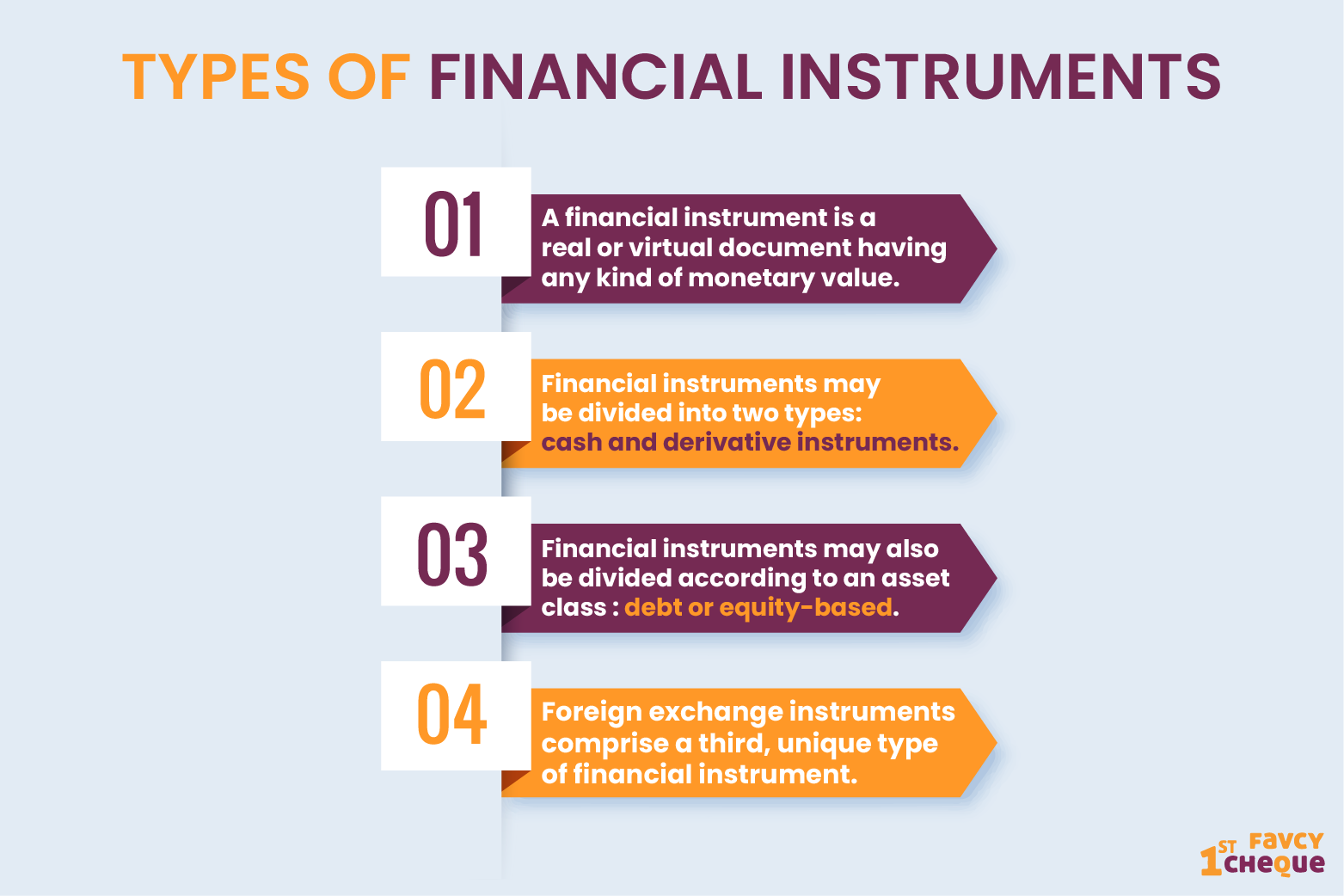

What is an investment instrument?

Investment instruments or financing instruments, in all their technicality, refer to documents such as a share certificate, promissory note, or bond, used as means to acquire equity capital or loan capital.

- A financial instrument is a real or virtual document representing a legal agreement involving any kind of monetary value.

- Financial instruments may be divided into two types: cash instruments and derivative instruments.

- Financial instruments may also be divided according to an asset class, depending on whether they are debt-based or equity-based.

To be in debt or not to be, is the question

Debt financing is a model that gains financing through loans and External Commercial Borrowings (ECBs) which invites a high rate of interest along with a pre-requisite for collateral. Since a majority of startups are volatile and unstable, debt financing is usually disregarded as a suitable option for such entrepreneurs.

On the other hand, equity financing is the preferred course of action for most startups. A private equity investor or venture capitalist invests in the shareholding of the company by way of subscribing to the equity share capital. This majorly helps in the expansion or diversification of the startup ventures.

While crowdfunding and incubation are some other rising forms of unconventional financing, investors prefer hybrid securities due to their secure nature.

So how does one go about equity financing?

Investment Instruments in Angel Investing

Financing is done by subscribing to Convertible Instruments such as Compulsory Convertible Preference Shares (CCPS) and Compulsory Convertible Debentures (CCD). These hybrid options are favourable as equity shareholding does not ensure a fixed return on investment and does not offer any special rights or preferences.

The most eminent investment instruments have been explained below -

- Compulsory Convertible Debentures (CCD)

These are 'deferred equity instruments' as they are mandatory to get converted into equity shares with a lapse in their maturity period. They are hybrid securities as they get converted from a debt (debenture) to an equity share and thus possess qualities of both.

The Companies Act exempts startups from taking valuation while raising funds using CCD hence, early-stage startups prefer CCD to raise funds when they are not in a situation to arrive at a fair valuation. CCD is the only instrument that allows startups to raise debt from an external party. CCDs are linked to Equity share which has to be compulsory converted into equity share on some pre-agreed trigger events. Thus, it can be deduced that they provide security to investors in the nature of debentures, and are ultimately rendered as shares, upon their conversion. According to Rule 2(1)(c) of the Deposit Rules, they can be issued provided they are converted to shares within 5 years of issue. The investors are generally compensated for their early risk by providing a certain discount percentage or putting a cap on the valuation of the startups.

If the start-up venture fails to deliver, the investors are still secured as they are bound to receive interest with a future promise of receiving dividends on the equity shares. Additionally, the start-up eventually has to merely issue shares without the burden of exhausting their cash flow. Furthermore, they promote foreign investment as opposed to certain other hybrid securities. Thus, their subscription proves beneficial to both parties most of the time.

However, there are certain downsides to the subscription of CCD's which is provoking investors to gradually shift to other hybrid securities. Whilst the initial purpose of this instrument was to curb the difficulty of valuation, the ventures are now required to obtain a 'Valuation Certificate' from the appropriate certifying officer at the time of investment. They also have to align with FEMA Guidelines, SEBI rules, FDI Regulations and Tax procedures. This severely increases the compliance requirements to be adhered to, which makes the investment procedure cumbersome.

- Compulsory Convertible Preferential Shares (CCPS)

Compulsory Convertible Preference Shares are the preferred choice and most favoured amongst investors for two main reasons -

-Dividend is first paid to preference shareholders, and the fixed amount of dividend gives them more.

– In case of liquidation, the preference shareholders have priority as per the waterfall mechanism.

Additionally, in case the business renders successful, the preference shares get converted to equity shares thereby increasing the scope of capital growth and profit retention of the investors.

The main privilege with these shares is their conversion linked with the performance of the company. This helps the private equity investors to balance any disparity in the valuation expectation of the venture, as the general valuation method renders inefficient in the case of start-ups due to the absence of a profit and loss account to show.

In this case, the investors chip in their resources when the company is at a lower valuation and eventually convert their shares to equity, which yields them a higher dividend, without pooling in additional resources when the venture has a higher valuation. Additionally, it benefits the start-ups to prevent the exhaustion of cash flow, as contrary to CCD, this security is not a 'debt’ or 'loan' which needs to be paid off with interest. This strikes a balance in the interests of the investors as well as the entrepreneurs.

However, like convertible debentures, this hybrid security is also infamous for its hefty load of compliance requirements and paperwork that is involved, mainly the pre-requisite for a valuation certificate.

All things considered, CCPS is the most used instrument for start-up investments currently, due to the liquidity advantage and repayment of share capital in an event of failure.

- Community Stock Option Pool (CSOP)

Community Stock Option Pool is not a security but an option to subscribe to the share of a company on a future date but on the price at which this CSOP has been vested. It works in the same way as ESOP for a company. If an investor buys a CSOP today and it is vesting at a trigger event, the investor will get the share at the time of the trigger event but at the price which was at the time, the CSOP was bought. The startup also has the right to repay back the money to the investor as per the increased valuation. CSOP doesn't come onto the cap table of a startups.

- Convertible Notes

Convertible notes are issued in the form of a 'debt instrument' to fund money to a venture in the way of a loan. The investor can convert this instrument into an equity share of the company, which is usually done at the time of the subsequent funding that the venture receives. This is based on a threshold set by the investor, which if not met, makes the venture liable to pay back the principal amount to the investor along with the accumulated interest.

Whilst the underlying principle of a convertible note is the same as that of a CCD, this instrument has proven less expansive and user-friendly due to the absence of several compliance requirements, mainly the valuation report and certificate.

Thus, the ventures which are unable to produce a substantial valuation report are also eligible to accumulate funding. However, as per the RBI Regulation and The Companies (Acceptance of Deposit) Rules, 2014, only 'recognised' start-ups are eligible to issue convertible notes in India. The transferability of these securities in India is in accordance with the exchange rules, which makes it mandatory to convert within a period of 5 years from the issue.

This instrument is believed to be highly efficient in terms of security, which on the one hand caters to the interest of investors, however also brings about a great deal of uncertainty to the start-ups as there is no assurance whether the investors will/will not convert their securities, as in the case of CCD and CCPS.

- Simple Agreement for Future Equity (SAFE)

SAFE is usually termed as an 'equity derivative contract' which converts the initial capital invested into the future stock of the company, based on contractual terms and conditions.

The primary reason for the success of SAFE in countries like USA, Singapore, Germany etc. is because there is no interest, unlike a debt instrument or loan. There is also no maturity date or compulsory period of conversion, leaving room for greater flexibility and negotiations. Instead of having terms and schedules, they are based in certain contingent events, the happening or non-happening of which determines the interest of the investor to either:

-Reclaim the invested principal amount or

-Convert the capital into stocks/shares of the

Furthermore, since it is a contract and not a security, it is fully regulated by the parties (investor and entrepreneur). This allows them to customize the clauses as per their situation, financial capabilities and proposed business model, thus striking a balance in the interest of both.

Lastly, since SAFE agreements don't have any interest or maturity date, they cannot be classified as a 'debt'. Likewise, due to the absence of dividend and other shareholder rights, it cannot be termed as 'equity' either. This makes the instrument non-reliable and less secure to a very large extent

Summing It Up

Following a thorough examination of the most notable hybrid instruments for start-up investments, it is clear that there is no 'one' certain method to take for all initiatives and investors. While some are concerned about onerous compliances, others may be concerned about the security or worth of the company.

As a result, it is important to assess the position of each instrument and choose the best investing strategy for you.

.png)

Here are the events of this week:

-

Eyewear unicorn Lenskart's subsidiary Neso Brands raises over $100M in seed round.

-

Tiger Global-backed GreyOrange raises $110 Mn in a growth-funding round.

-

Smytten raises $15M in pre-Series B round.

|